By David Lazarus, Los Angeles Times, October 11, 2013

The richest 1% own nearly half of all global wealth.

Let’s get our heads around that. Only a tiny fraction of the roughly 7 billion people in the world accounts for 46% of the estimated $241 trillion in money, property and other material resources available.

The richest 10%, meanwhile, can claim 86% of global wealth, leaving 90% of the world’s population to divvy up whatever’s left.

These extraordinary figures were included in a report this week from Credit Suisse Research Institute. It found that the gravy train is chugging along, but with relatively few passengers.

Former Labor Secretary Robert Reich has been sounding the alarm over wealth inequality for years. He’s at the center of a recent documentary, “Inequality for All,” which explains the problem in frightening detail.

“When so much of the purchasing power, so much of the economic gain, goes to the very top,” Reich told me, “there’s simply not enough purchasing power in the rest of the economy.”

That has profound implications. In the United States, consumer spending accounts for about 70% of all economic activity. If most consumers are getting by with less, the inevitable outcome is that they’ll have fewer dollars to pump into the economy.

Reich noted that wealth inequality was greatest in this country in 1928 and 2007. In both years, the top 1% represented about a quarter of total income.

And shortly thereafter, in 1929 and again in 2008, the U.S. economy tanked, dragging down the rest of the world with it.

Other nations, Reich said, have taken steps to address wealth inequality. They’ve invested more in infrastructure and education in an effort to create more economic opportunities throughout the social spectrum.

The United States, for its part, has been content to let the problem grow.

“We are far more unequal than any other advanced society in the world, and we are surging toward greater and greater inequality,” Reich said.

The Credit Suisse report bears that out. Average adult wealth in Switzerland is $513,000, the world’s highest, followed by Australia ($403,000), Norway ($380,000) and Luxembourg ($315,000).

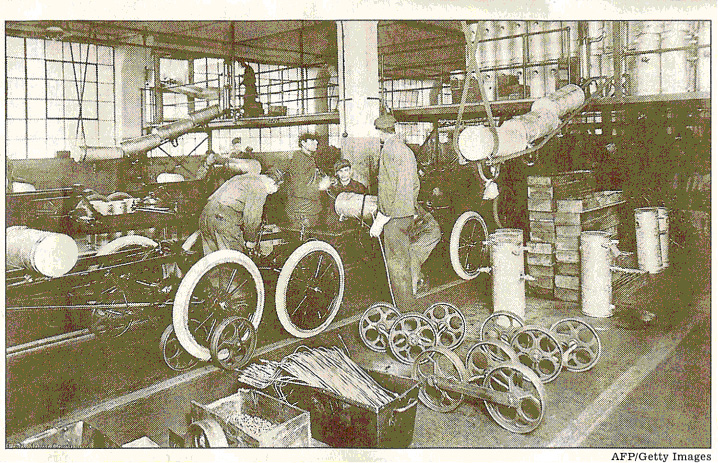

IN 1914, HENRY FORD more than doubled factory workers’ minimum pay so they could afford to buy Ford cars. Above is the Highland Park plant in 1913.

——————————————————————————————————

Average adult wealth in the United States is $301,000, but that number is heavily skewed by the fact that this country has, by far, the greatest number of “ultra-high net worth” individuals, with personal assets exceeding $50 million.

According to the report, the United States accounts for 46% of all such superwealthy people worldwide. Coming in a distant second is China, which boasts 6% of the world’s super rich.

Being successful, obviously’ isn’t a bad thing. There’s much to be said for the whole land-of-opportunity idea, in which people are rewarded for a job well done.

But that’s not what’s actually happening. The rich are gaming the system so they can accumulate a greater share of wealth to the detriment of others.

They do this by using their financial (and hence political) clout to reduce their share of taxes, thus placing a greater burden on the rest of society to fund government programs and the public sector’s investment in economic growth.

The top marginal tax rate for much of the 1920s was 25%. It was 35% in 2007. At both times, wealth inequality was at record levels.

Compare that with the 1950s when, under then President Dwight Eisenhower, a Republican, the top marginal tax rate was 91%. Were the upper classes barely scraping by with such an onerous tax load?

Hardly. This period was one of the most prosperous in American history. Not coincidentally, wealth inequality was at a low as almost everyone shared in the economy’s and the country’s good fortune.

In contemporary terms, job creators were paying much higher taxes than working stiffs, and – guess what? – there were still plenty of jobs being created.

“I’m sure the rich in the 1950s would have preferred a 10% tax rate,” said Gregory Clark, an economist at UC Davis. “But there’s no empirical evidence that taxing the rich slows down economic growth.”

Just the opposite. Since consumer spending is required for growth, placing more money in the hands of consumers would seem crucial to fueling economic expansion, which, it goes without saying, has the ancillary benefit of helping the rich get richer.

Henry Ford recognized this. In 1914, he more than doubled factory workers’ minimum pay to $5 a day ($1l7 in today’s dollars). In part, this was to halt costly employee turnover. But it was also to provide workers with enough cash to buy the cars they were making.

“It is our belief that social justice begins at home,” said James Couzens, Ford’s treasurer at the time. “We want those who have helped us to produce this great institution and are helping to maintain it to share our prosperity.

“We want them to have present profits and future prospects,” he said. “Believing as we do that a division of our earnings between capital and labor is unequal, we have sought a plan of relief suitable for our business.”

U. S. chief executives made an average of$12.3 million last year, or 354 times what the average rank-and-fIle worker pulled down, according to the AFL-CIO. Thirty years ago, the average CEO was paid 42 times what ordinary workers received.

The Credit Suisse report shows that the number of millionaires worldwide has risen by almost 2 million since the middle of last year. There are now about 99,000 individuals worth more than $50 million apiece.

Yet two-thirds of all other adults have assets worth less than $10,000. Put another way, two-thirds of all adults worldwide represent no more than 3% of global wealth.

Credit Suisse forecasts that global wealth will rise almost 40% over the next five years. That’s the good news.

The bad news is that you, and billions of other hardworking people, will see little if any of those gains.